For years, the biggest obstacle preventing stablecoins from becoming mainstream financial infrastructure was never technology.

For years, the biggest obstacle preventing stablecoins from becoming mainstream financial infrastructure was never technology.

It was trust.

Banks questioned their regulatory status.

Institutional investors worried about custody and compliance.

Governments remained concerned about systemic financial risks.

While stablecoins proved they could move billions of dollars across blockchain networks every day, they still operated outside the traditional banking system.

That may have changed.

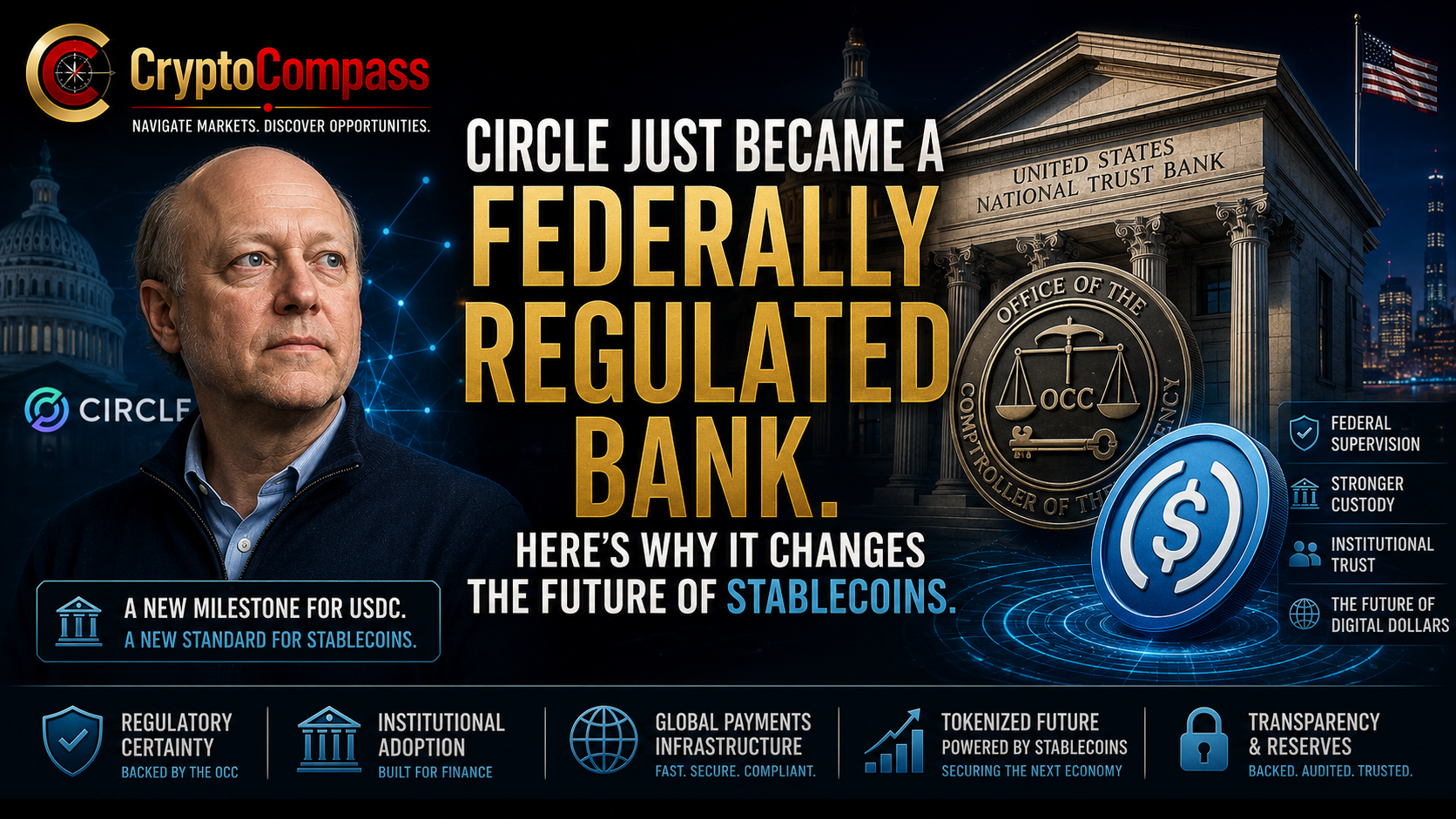

Circle, the issuer of USDC, has officially received final approval from the Office of the Comptroller of the Currency (OCC) to establish a national trust bank in the United States.

The announcement may appear administrative on the surface.

In reality, it could become one of the most important regulatory milestones in the history of the stablecoin industry.

Because this is no longer simply about one company obtaining another license.

It is about digital dollars becoming part of America's regulated financial infrastructure.

Stablecoins Are Growing Up

The first generation of stablecoins was designed primarily for cryptocurrency trading.

They allowed investors to move capital between exchanges without relying on traditional banking systems.

Over time, their role expanded dramatically.

Today, stablecoins facilitate international payments, decentralized finance, tokenized securities, institutional settlement, corporate treasury management and cross-border commerce.

According to industry data, stablecoins now process transaction volumes that rival or exceed major global payment networks during certain periods.

They are no longer merely crypto assets.

They are becoming digital payment infrastructure.

However, one problem has persisted.

Most stablecoin issuers were not banks.

That distinction has mattered far more than many investors realized.

Why An OCC Charter Matters

The Office of the Comptroller of the Currency is one of the primary federal banking regulators in the United States.

Receiving approval to operate as a national trust bank places Circle under direct federal supervision for its trust banking activities.

For institutional investors, this fundamentally changes the conversation.

Instead of evaluating USDC solely as a cryptocurrency product, financial institutions can increasingly evaluate Circle as a federally supervised financial institution operating within a well-established regulatory framework.

That distinction reduces one of the largest barriers preventing broader institutional adoption.

Regulation is often viewed as an obstacle within crypto.

For institutions, regulation is frequently a prerequisite.

The Regulatory Race Has Replaced The Technology Race

During crypto's first decade, competition focused almost entirely on technology.

Which blockchain was faster?

Which protocol was cheaper?

Which stablecoin had the largest market capitalization?

Those questions still matter.

But the next competitive advantage appears increasingly regulatory rather than technical.

Circle's approval demonstrates that obtaining trusted regulatory status may become just as valuable as launching new blockchain products.

In the coming years, stablecoin issuers are likely to compete on transparency, compliance, reserve management and banking relationships as aggressively as they compete on transaction volume.

Wall Street Wants Regulatory Certainty

The timing is significant.

Over the past two years, nearly every major financial institution has accelerated its digital asset strategy.

BlackRock launched tokenized money market funds.

Franklin Templeton expanded blockchain investment products.

JPMorgan continues developing blockchain settlement infrastructure.

Fidelity has increased its digital asset offerings.

Banks around the world are experimenting with tokenized deposits and blockchain-based payments.

None of these institutions are seeking regulatory ambiguity.

They are seeking regulatory certainty.

Circle's approval moves the stablecoin industry closer to that objective.

Stablecoins Are Becoming The Foundation Of Tokenized Finance

One of the most important developments in financial markets is the rapid growth of tokenization.

Governments are exploring tokenized bonds.

Asset managers are issuing tokenized money market funds.

Private equity firms are evaluating tokenized ownership structures.

Real estate platforms are experimenting with fractional digital ownership.

Every one of these markets requires a reliable settlement asset.

Stablecoins are increasingly filling that role.

Rather than serving only cryptocurrency exchanges, stablecoins are becoming programmable digital cash for global financial markets.

If tokenization expands over the next decade as many analysts expect, stablecoins may become one of the most important components of that ecosystem.

This Is Bigger Than Circle

The significance of this approval extends beyond a single company.

It signals a broader shift in the relationship between regulators and digital assets.

For years, crypto firms attempted to avoid traditional financial regulation.

Today, many of the industry's largest companies are actively pursuing banking licenses, trust charters and regulated financial status.

Rather than replacing the banking system, crypto infrastructure is beginning to integrate with it.

This evolution could prove far more important than many headline-grabbing token launches or short-term market rallies.

Infrastructure rarely attracts the most attention.

Yet infrastructure often creates the greatest long-term value.

What It Means For Investors

For investors, Circle's approval represents more than positive news for USDC.

It provides another signal that stablecoins are gradually transitioning from crypto-native instruments into globally regulated financial products.

That evolution could unlock broader institutional participation, encourage deeper integration with traditional banks and strengthen confidence in blockchain-based payment infrastructure.

Markets often focus on prices.

History tends to remember infrastructure.

The approval of a federally regulated trust bank may not move markets overnight.

But years from now, it could be remembered as one of the moments when stablecoins stopped being viewed as experimental crypto products and started becoming part of the modern financial system.

CryptoCompass View

The future of stablecoins will not be determined solely by transaction speed or market capitalization.

It will be determined by trust.

Circle's OCC approval demonstrates that the industry's next stage is not simply decentralization.

It is institutionalization.

Crypto is no longer trying to replace traditional finance.

Increasingly, it is becoming part of it.

As blockchain infrastructure continues to mature, regulated stablecoins may emerge as the digital cash layer supporting tokenized assets, cross-border payments and the next generation of global capital markets.

The stablecoin race has entered a new phase.

And this time, regulation may become the industry's greatest competitive advantage.