Crypto commentator Jussy reopened the HYPE versus ASTER debate with a simple but sharp comparison: Hyperliquid generated more than $1.3 billion in protocol fees, with nearly all of that value

Crypto commentator Jussy reopened the HYPE versus ASTER debate with a simple but sharp comparison: Hyperliquid generated more than $1.3 billion in protocol fees, with nearly all of that value routed toward HYPE buybacks, while Aster generated more than $450 million in fees and promoted a major ASTER buyback program.

On the surface, both models look similar. Both perpetual DEXs turned trading activity into token demand. Both used protocol revenue to support their native asset. Both tried to prove that DeFi tokens can capture real cash flow instead of relying only on emissions, points or speculative narratives.

Source: @jussy_world on X

The market has treated them very differently.

The reason is not only that Hyperliquid is larger or that its buyback number is higher. The cleaner explanation is alignment. HYPE was built around users and holders first. ASTER has faced a much harder market read because buybacks have been set against unlocks, insider-aligned supply pressure and a token structure that traders increasingly view as less friendly to ordinary holders.

Hyperliquid Built A User-Holder Flywheel

Hyperliquid’s advantage starts with distribution. HYPE launched with a large community allocation and no private-investor allocation at genesis, which gave early users a direct stake in the protocol’s growth. That matters because the people trading, promoting and building around Hyperliquid were also the people rewarded by the token.

The fee loop then made that alignment stronger. Hyperliquid’s Assistance Fund routes the overwhelming majority of perp and spot-orderbook revenue into HYPE purchases. DeFiLlama’s current methodology lists 99% of relevant trading fees going to the Assistance Fund for buying HYPE, turning exchange activity into a constant structural bid for the token.

That is why HYPE’s buybacks feel different from a normal support program. They are not just a marketing answer to price weakness. They are part of the product’s holder-value design. More trading creates more fees. More fees create more buybacks. More buybacks support HYPE. A stronger HYPE token helps keep attention, liquidity and ecosystem confidence around Hyperliquid.

That same loop also supports Hyperliquid’s broader expansion beyond perps. Its 2025 annual report story showed a protocol moving toward a full onchain exchange stack, with perps, spot markets, HyperEVM activity and new market structures feeding the same ecosystem.

Aster’s Buybacks Ran Into Supply Pressure

Aster’s problem is not the absence of revenue. Its reported fee base is large, and its official tokenomics include a protocol-revenue buyback initiative. The issue is that buybacks only help holders when they beat the supply coming the other way.

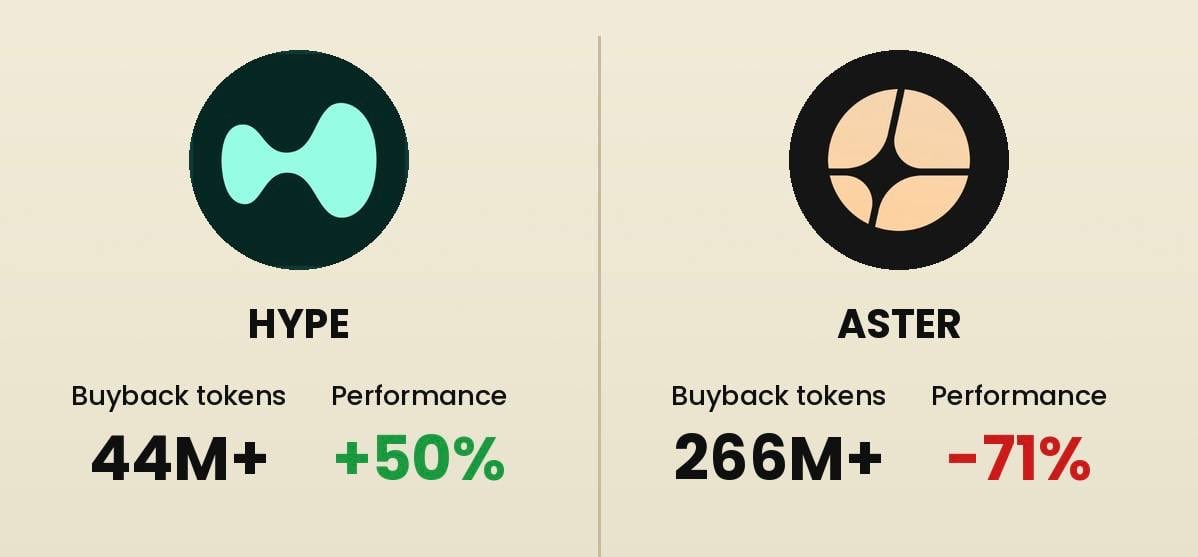

That is the key point in Jussy’s later chart-driven update. The post framed the difference as “No VCs, No insiders” for HYPE, while noting that ASTER had bought back 266 million tokens but had 960 million unlocks since TGE. In that framing, ASTER’s buybacks did not create the same holder flywheel because the market saw too much token supply arriving from the other side.

That is also why Aster’s earlier roughly $4 million-per-day buyback push never solved the market’s deeper concern. Big buybacks can slow sell pressure, but they cannot automatically create trust if holders believe insiders, unlocks or early allocations are selling into the same demand.

This is where ASTER and HYPE split. HYPE’s structure made users feel like the protocol’s revenue was working for them. ASTER’s structure left the market asking whether buybacks were mostly absorbing supply from earlier allocations.

The Market Is Rewarding Alignment, Not Just Revenue

The HYPE versus ASTER debate is now bigger than one chart. It is a test of what crypto investors actually reward when protocols generate real fees.

Revenue helps. Buybacks help. But holder alignment decides whether the market treats those buybacks as value capture or as exit liquidity. Hyperliquid has so far convinced traders that protocol growth flows back to users and holders. Aster has not won that trust at the same level, even with large fees and aggressive repurchases.

That is why the “one worked and the other didn’t” argument lands. HYPE’s buyback model sits inside a user-first distribution story, a dominant perp DEX, deep liquidity and visible fee capture. ASTER’s buyback story keeps running into unlock math and insider-supply doubts.

The next phase will be decided by whether Aster can prove that fee revenue consistently benefits holders after unlocks, emissions and early-supply pressure are counted. Until then, Hyperliquid has the cleaner market structure: users trade, the protocol earns, HYPE gets bought, and holders can see why the flywheel exists.

The post HYPE And ASTER Show Why Buybacks Fail When VCs Outrun Holders appeared first on Crypto Adventure.