Airwallex, Revolut, and Stripe didn’t reinvent finance. They just fixed things that banks had stopped bothering to fix. Once settlement speed, global reach, and transaction costs became part

Airwallex, Revolut, and Stripe didn’t reinvent finance. They just fixed things that banks had stopped bothering to fix. Once settlement speed, global reach, and transaction costs became part of the product itself — not wallpaper on top of it — everything else followed.That is why Revolut now serves more than 70 million customers, while Stripe processes transaction volumes through its infrastructure that are comparable to a meaningful share of the global economy.

The same pressure is now building at the edge between traditional finance and crypto. For years the two ran on separate tracks, but now that’s changing. Stablecoin transfers and crypto-to-fiat conversion are getting folded into the same infrastructure that handles everything else. Which means On/Off Ramps — the points where capital moves in and out of digital finance — are no longer a technical afterthought. They’re where conversion rates are won or lost, users decide whether to stay or leave, and where the actual economics of a product get determined.

Why Your Ramp Infrastructure Is Quietly Deciding Your 90-Day Retention

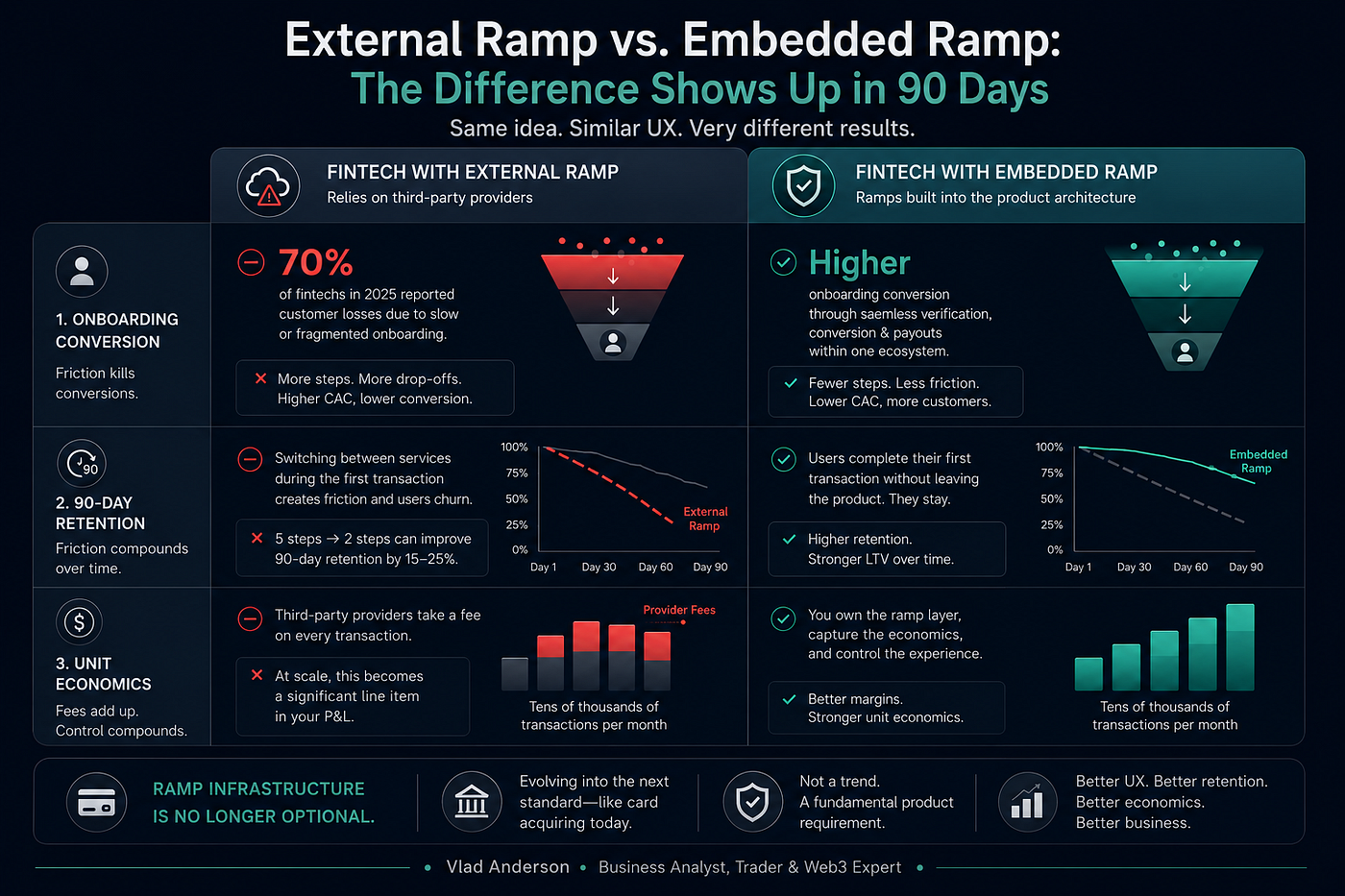

Imagine two fintech products with the same core idea and a similar UX. The first relies on a third-party ramp provider: conversion happens somewhere “outside” the product, and any outage or delay automatically becomes the customer’s problem. The second has built the ramp layer directly into its architecture: onboarding, conversion, and payouts all happen within a single ecosystem. The difference between the two is not obvious on launch day. It becomes obvious 90 days later when you look at retention.

The first place this shows up is onboarding conversion. Every additional step in verification or conversion causes a portion of users to drop off and never return. Seven in ten fintech companies reported losing customers in 2025 because their onboarding was too slow or fell apart halfway through. Which makes the CAC math brutal — you paid to get those users, they just never converted.

The second area is 90-day retention. A customer who does not have to switch between services during their first transaction is more likely to stay — not because of loyalty, but simply because they never felt the need to look for an alternative. A product with an external ramp layer introduces friction precisely when users are trying to complete a task, and that friction accumulates over time.

The third area is unit economics. An external provider takes a fee from every transaction, while an embedded solution allows the platform to control that layer itself. At tens of thousands of transactions per month, the difference stops being theoretical and becomes a line item in the P&L. The quality of ramp infrastructure is evolving toward what card acquiring is today — not a trend but a fundamental product requirement.

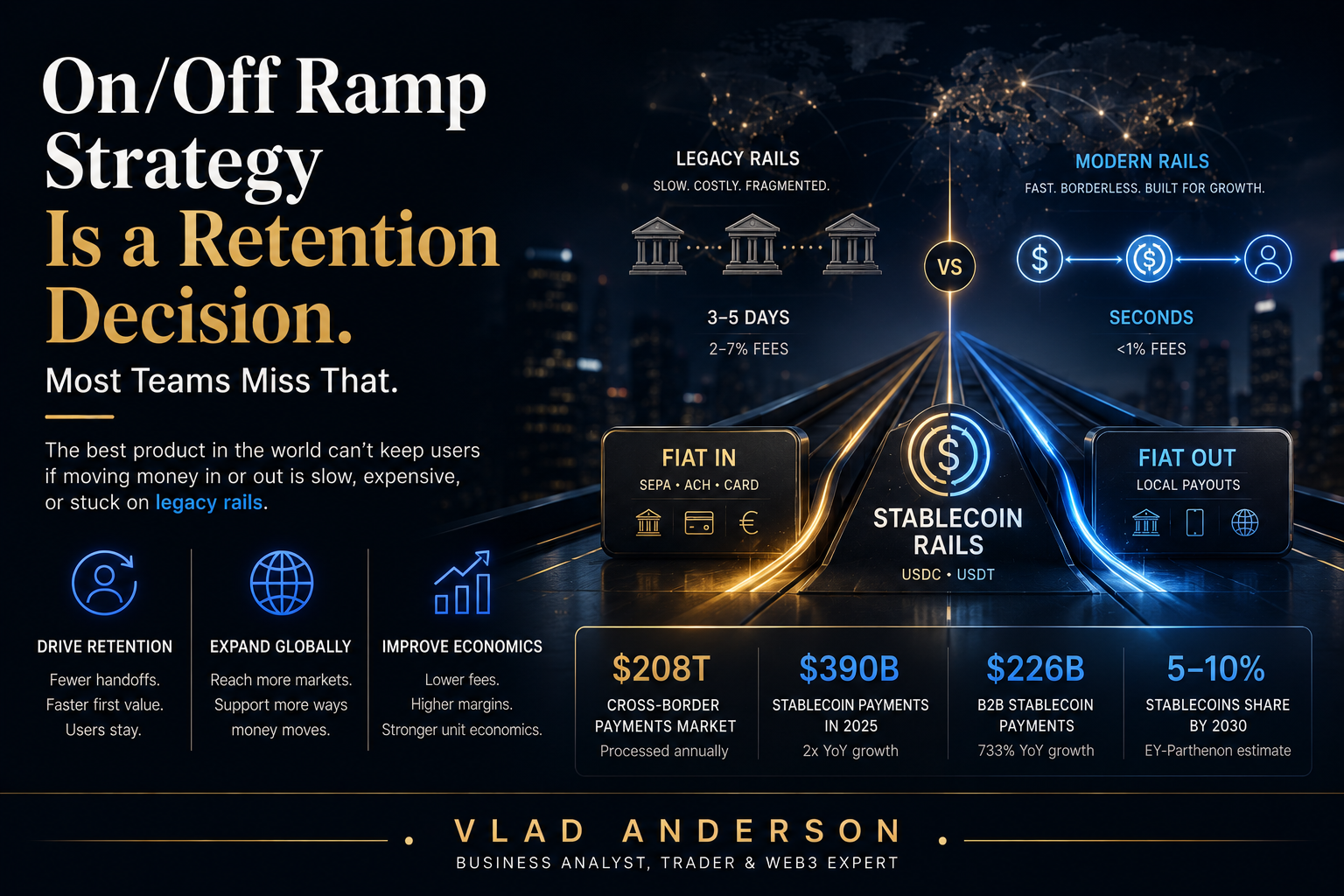

$208 Trillion Still Moves on 1970s Rails — Here’s What’s Replacing Them

The global cross-border payments market processes $208 trillion annually, yet most of that money still moves through infrastructure built in the 1970s. A SWIFT transfer between two countries typically takes 3–5 business days, while correspondent banks absorb between 2% and 7% in fees depending on the corridor. In regions without direct banking relationships — Latin America, Southeast Asia, and parts of Africa — traditional rails are not only expensive but increasingly unable to keep up with demand.

Cards have partially solved this problem for consumers. However, B2B settlements and payouts to international partners still rely heavily on bank transfers, with all the delays and friction that come with them. Stablecoins don’t replace banks — they fill the gaps where banks are just too slow or too expensive.

According to McKinsey and Artemis Analytics, real stablecoin payment volume reached $390 billion in 2025, more than double the previous year’s figure. Of that amount, $226 billion came from B2B transactions, representing 733% year-over-year growth. This is not speculative activity: these are vendor payments, cross-border payouts, and settlements between different jurisdictions.

The flow is relatively straightforward: fiat comes in via SEPA, ACH, or card — gets converted to USDC or USDT — moves across borders in seconds — then converts back to fiat on the other side. That’s the model behind Bridge (acquired by Stripe for $1.1B in late 2024), Mural Pay, and others building B2B rails on stablecoins. SEPA and ACH aren’t going anywhere; they’re still the on and off ramps. The stablecoin is just what happens in the middle, where banks are either too slow or too costly to be useful.

Which On/Off-Ramp Provider Actually Fits Your Product?

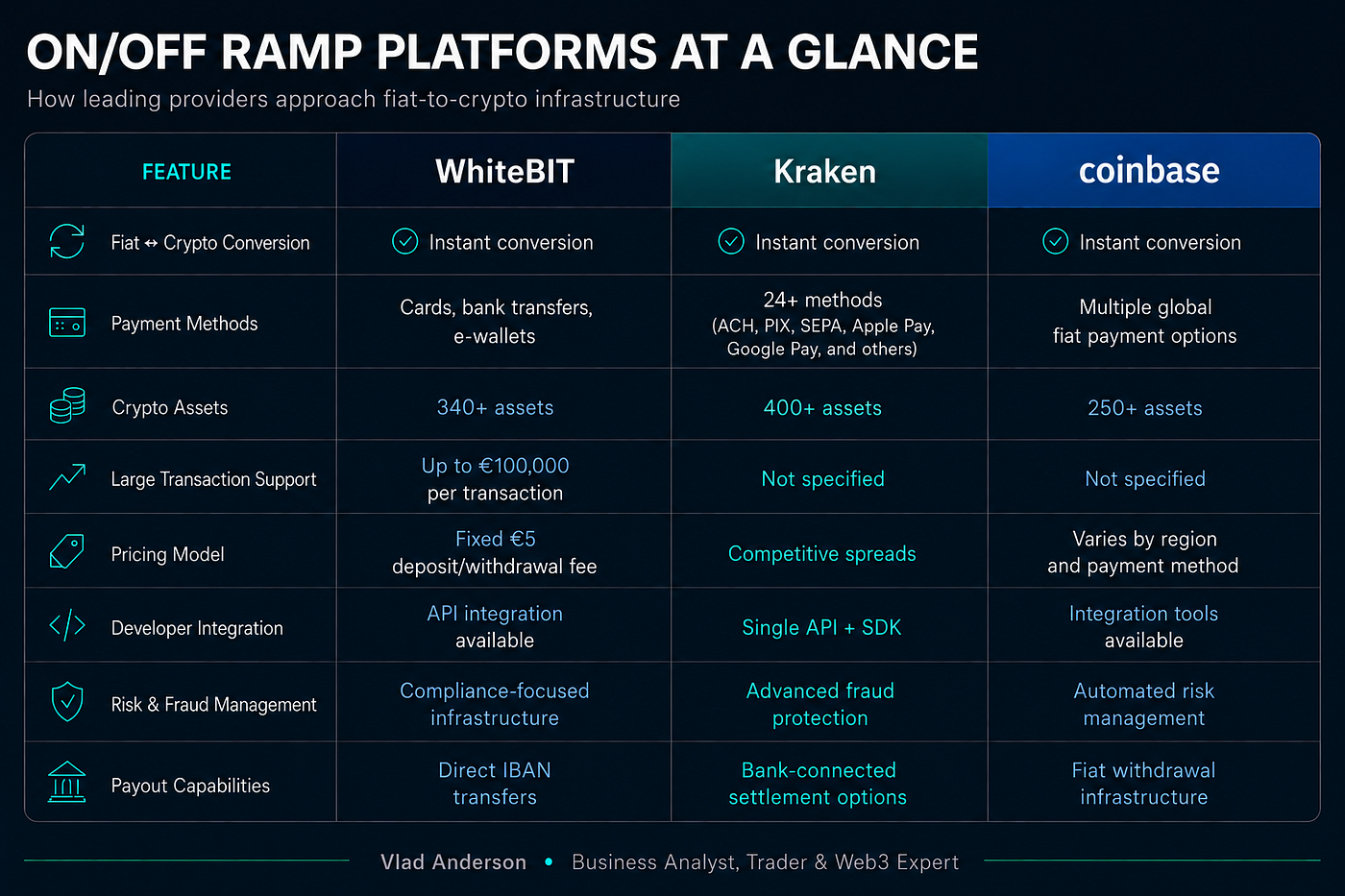

Choosing a ramp provider is not about finding a universally “best” solution on the market. First and foremost, it is about finding the right fit for a specific business model, user geography, and operational requirements. Each of the platforms below addresses different needs, so understanding the context in which they are used is far more important than comparing individual features in a table.

WhiteBIT appears to be the most logical choice for fintech and B2B products operating within the SEPA region, where users regularly handle large transaction volumes. In such scenarios, the fee structure has a direct impact on unit economics, meaning that lower transaction costs can generate a significant financial benefit at scale.

Kraken is well suited for teams looking to simplify the integration of fiat-to-crypto infrastructure while avoiding the additional costs of building their own payment logic. It is a practical option for products where the ramp should remain a supporting service rather than a standalone area of development.

Coinbase delivers the strongest value proposition for products targeting a broad retail audience. If the primary goal is to minimize onboarding friction and provide the smoothest possible first-time experience for users with little or no cryptocurrency background, Coinbase’s solution addresses this challenge at the product architecture level.

So,

If a product handles international transfers or currency conversion, the question of a ramp strategy is already relevant — even if the team doesn’t call it that yet. Postponing it means postponing work on retention, profitability, and the overall quality of the payment experience.

Each model comes with trade-offs. White-label is the fastest path to launch — minimal dev work, but less control over what you actually ship. API-first gives you the most flexibility, and it costs you in engineering time. A licensed provider handles compliance and regulatory work for you, which is the main reason to go that route.

According to EY-Parthenon estimates, stablecoins could account for 5–10% of the cross-border payments market by 2030. This is not about every fintech company moving into crypto. It is about ramp infrastructure gradually becoming part of the core payments architecture and understanding it becoming an essential component of controlling transaction economics and the customer journey.

Disclaimer: This is not financial or investment advice. Do your own research before making any decisions. Use at your own risk.