Markets5 min read

Monthly Report | Part IV — Looking Ahead: What July Could Change

Geopolitical tensions reminded investors that global markets remain vulnerable to external shocks.

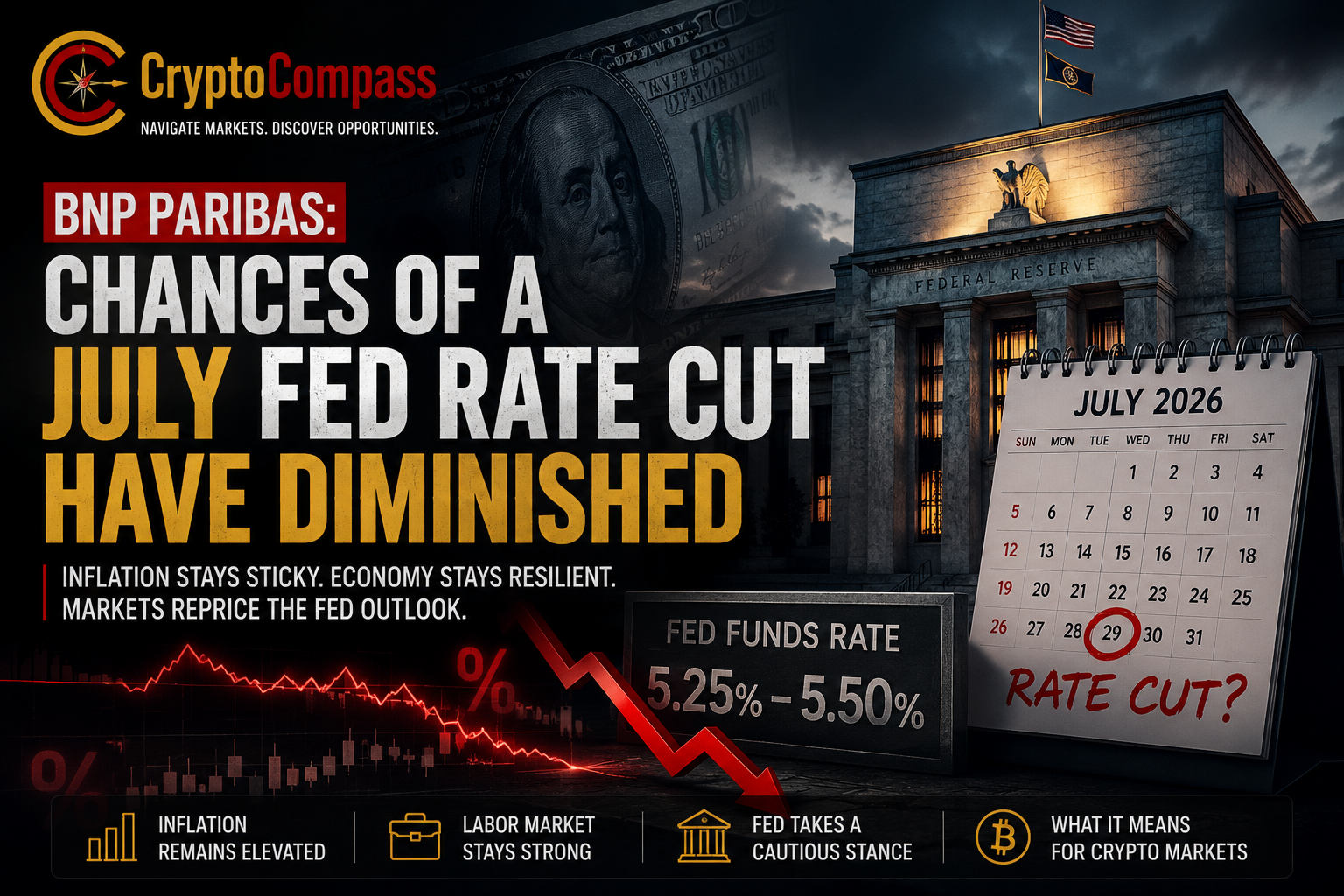

BNP Paribas believes the likelihood of a Federal Reserve rate cut in July has declined as inflation remains persistent and the U.S. economy continues to show resilience.

Just weeks ago, investors were increasingly convinced that the Federal Reserve would begin cutting interest rates as early as July.

That optimism is now fading.

According to BNP Paribas, recent economic developments have significantly reduced the probability of a July rate cut, reinforcing the view that the Fed is likely to keep interest rates higher for longer while waiting for clearer evidence that inflation is firmly under control.

The reassessment comes at an important moment for global financial markets. Interest-rate expectations remain one of the largest drivers of capital flows across equities, bonds, commodities and digital assets.

Although inflation has eased considerably from its peak in 2022, policymakers continue to stress that progress toward the Federal Reserve's 2% target remains incomplete.

Core inflation remains elevated.

Consumer spending has held up better than expected.

The labor market continues to show resilience despite restrictive monetary policy.

Taken together, these factors reduce the urgency for policymakers to begin easing financial conditions.

Federal Reserve officials have repeatedly stated that they would rather wait longer than risk cutting rates too early and allowing inflation to accelerate again.

BNP Paribas believes recent data support that cautious approach.

The phrase "higher for longer" has once again become the dominant narrative across global markets.

If investors conclude that interest rates will remain elevated throughout the summer, financial conditions are likely to stay restrictive.

That has several implications:

Government bond yields could remain elevated.

The U.S. dollar may continue to find support.

Liquidity conditions could remain tighter than many investors anticipated earlier this year.

Risk assets may struggle to attract aggressive new capital.

Markets are therefore becoming increasingly sensitive to every major economic release, particularly inflation and employment data.

For the cryptocurrency market, Federal Reserve policy remains one of the most influential macroeconomic variables.

Lower interest rates generally encourage investors to increase exposure to higher-risk assets by improving liquidity and reducing borrowing costs.

Delayed rate cuts can slow that process.

However, today's crypto market is structurally different from previous cycles.

Unlike 2022, Bitcoin is no longer driven primarily by speculative retail demand.

Institutional participation has expanded significantly through spot Bitcoin ETFs, corporate treasury accumulation and growing integration with traditional financial markets.

As a result, macro policy still matters—but its impact is increasingly being balanced by long-term structural demand.

This helps explain why Bitcoin has shown greater resilience than many altcoins during recent periods of macro uncertainty.

The outlook for July will ultimately depend on incoming economic data.

Investors will closely monitor:

U.S. Consumer Price Index (CPI)

Nonfarm Payrolls

Unemployment rate

Wage growth

ISM manufacturing and services surveys

Public remarks from Federal Reserve officials

Any meaningful deterioration in economic activity could revive expectations for an earlier rate cut.

Conversely, stronger inflation or employment data would reinforce the "higher for longer" scenario.

BNP Paribas' latest assessment reflects a broader shift in market psychology rather than a sudden change in Federal Reserve policy.

Markets are recognizing that inflation remains the Fed's primary concern, even as economic growth moderates.

For crypto investors, this means liquidity expectations should remain measured in the short term.

Nevertheless, Bitcoin's growing institutional adoption continues to provide an important structural tailwind that was largely absent during previous tightening cycles.

The path of interest rates will continue to influence market sentiment, but the long-term investment case for digital assets is increasingly being shaped by institutional capital, regulatory clarity and expanding financial infrastructure rather than monetary policy alone.