U.S. Federal Housing Director Says Bitcoin Is Making Homes More Affordable

USDA

USDA

USDA

BTC

USDA

BTC

USDA

USDA

READ

READ

FHFA Director Bill Pulte has ordered Fannie Mae and Freddie Mac to prepare their systems to count cryptocurrency as a qualifying asset for mortgage applications, a directive that could open homeownership to millions of crypto holders currently locked out of traditional lending.

Federal Housing Director Links Bitcoin to Lower Home Prices

Pulte announced the order on X, stating he had directed "the Great Fannie Mae and Freddie Mac to prepare their businesses to count cryptocurrency as an asset for a mortgage" after what he described as "significant studying." The directive explicitly cites President Trump's stated goal of making the United States "the crypto capital of the world."

After significant studying, and in keeping with President Trump's vision to make the United States the crypto capital of the world, today I ordered the Great Fannie Mae and Freddie Mac to prepare their businesses to count cryptocurrency as an asset for a mortgage.

— Pulte (@pulte) June 25, 2025

SO ORDERED pic.twitter.com/Tg9ReJQXC3

Source: @pulte on X

This is not a study or a pilot. The directive explicitly orders the two government-sponsored enterprises to prepare their businesses for crypto-asset integration, making it a binding operational mandate from the agency that oversees both entities.

That order is now producing concrete results. On March 26, 2026, Fannie Mae announced it will accept crypto-backed mortgages for the first time through a partnership between mortgage lender Better Home & Finance and crypto exchange Coinbase.

Under the new program, homebuyers can pledge Bitcoin or stablecoin holdings as collateral for a separate down payment loan without selling their crypto. That structure avoids triggering capital gains taxes while the borrower takes out a traditional 15- or 30-year mortgage.

Why Counting Crypto as a Mortgage Asset Changes the Game

The significance lies in who this policy targets. Roughly 65 million Americans, about 20% of the population, now own cryptocurrency. Of those, 74% hold portfolios under $50,000.

These are not wealthy investors looking for portfolio diversification. They are disproportionately Gen Z and Millennial holders who report 25% of their portfolios in non-traditional assets, many of whom have been unable to convert crypto gains into a traditional down payment without liquidating at a tax penalty.

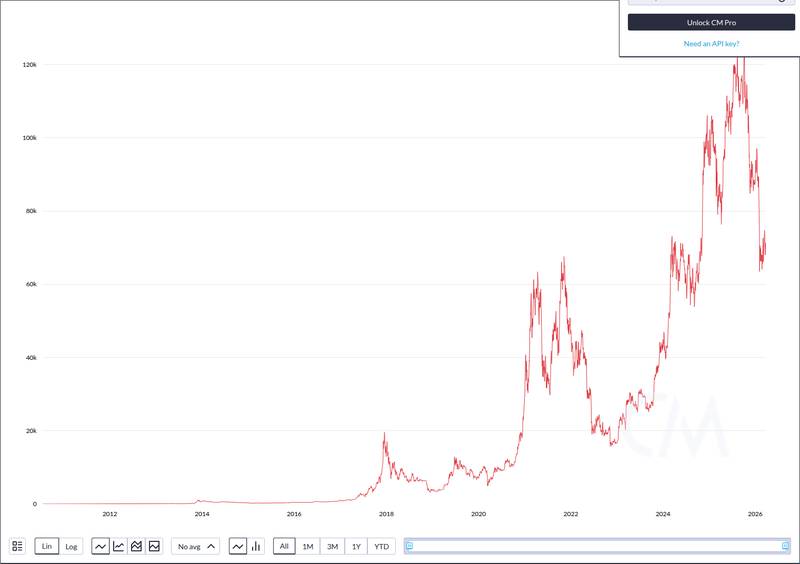

Bitcoin was trading at $65,924 on March 27, 2026, with a market cap of $1.32 trillion. The price sits roughly 46% below its October 2025 all-time high of $126,080, down 4.45% over 24 hours.

The Fear & Greed Index reads 13, deep in "Extreme Fear" territory. Yet the FHFA directive represents a structural adoption signal that operates independently of short-term price action.

Max Branzburg, Head of Consumer and Business Products at Coinbase, framed the move in generational terms:

"Token-backed mortgages are a major first step to unlocking homeownership for the younger generations that have struggled with barriers to saving for a traditional down payment."

Max Branzburg, Coinbase, via Fortune

The scale of federal mortgage programs underscores the potential reach. In 2024 alone, the FHA issued over 760,000 mortgages worth $230 billion. If crypto-asset qualification extends beyond Fannie and Freddie to FHA, VA, and USDA lending programs, the addressable pool of eligible crypto holders expands dramatically.

Bitcoin and Real Estate: From Fringe Idea to Federal Policy

One important distinction: Pulte's order only covers assets held on U.S.-regulated centralized exchanges subject to all applicable laws. Decentralized holdings, self-custodied wallets, and offshore exchange balances do not qualify.

Implementation also requires Fannie Mae and Freddie Mac to build entirely new underwriting infrastructure before the policy goes fully live. The Better/Coinbase partnership is the first concrete product, but broader rollout depends on how quickly the GSEs can integrate crypto-asset verification into their existing systems.

Bitcoin's on-chain network activity provides additional context for the structural trend underpinning this policy shift. With over 65 million Americans holding crypto and network fundamentals remaining stable despite a 46% drawdown from all-time highs, the case for treating digital assets as legitimate mortgage collateral rests on more than price alone.

The headline framing deserves a caveat. According to unconfirmed editorial characterizations, the story was presented as "Bitcoin is making homes more affordable." Pulte's actual statements focus on counting crypto as an asset for mortgage qualification, not on affordability directly. The policy removes a barrier for crypto holders, but it does not lower home prices.

Currently, FHA, VA, and USDA federal lending programs do not permit cryptocurrency as collateral or down payment documentation. Whether Pulte's directive eventually extends to those programs remains an open question with no announced timeline.

The FHFA oversees both Fannie Mae and Freddie Mac, meaning Pulte's directive is binding on the two entities that guarantee the vast majority of U.S. mortgages. For the 65 million Americans holding crypto, the gap between digital wealth and traditional homeownership just narrowed.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency and digital asset markets carry significant risk. Always do your own research before making decisions.

Read original article on tokentopnews.com